The $1,500 Annual Maximum: The 1970s Standard That's Quietly Robbing Your Patients (and Your Practice)

Let’s take a quick trip back to 1970.

The Beatles were breaking up, bell-bottom jeans were a "fashion choice," and the average price of a new home was about $24,000. In that same year, dental insurance companies rolled out a revolutionary new concept: the $1,500 annual maximum.

At the time, it was a generous safety net. It covered almost any major dental catastrophe you could dream up. You could get your crowns, your root canals, and probably buy the dentist a steak dinner with the change left over.

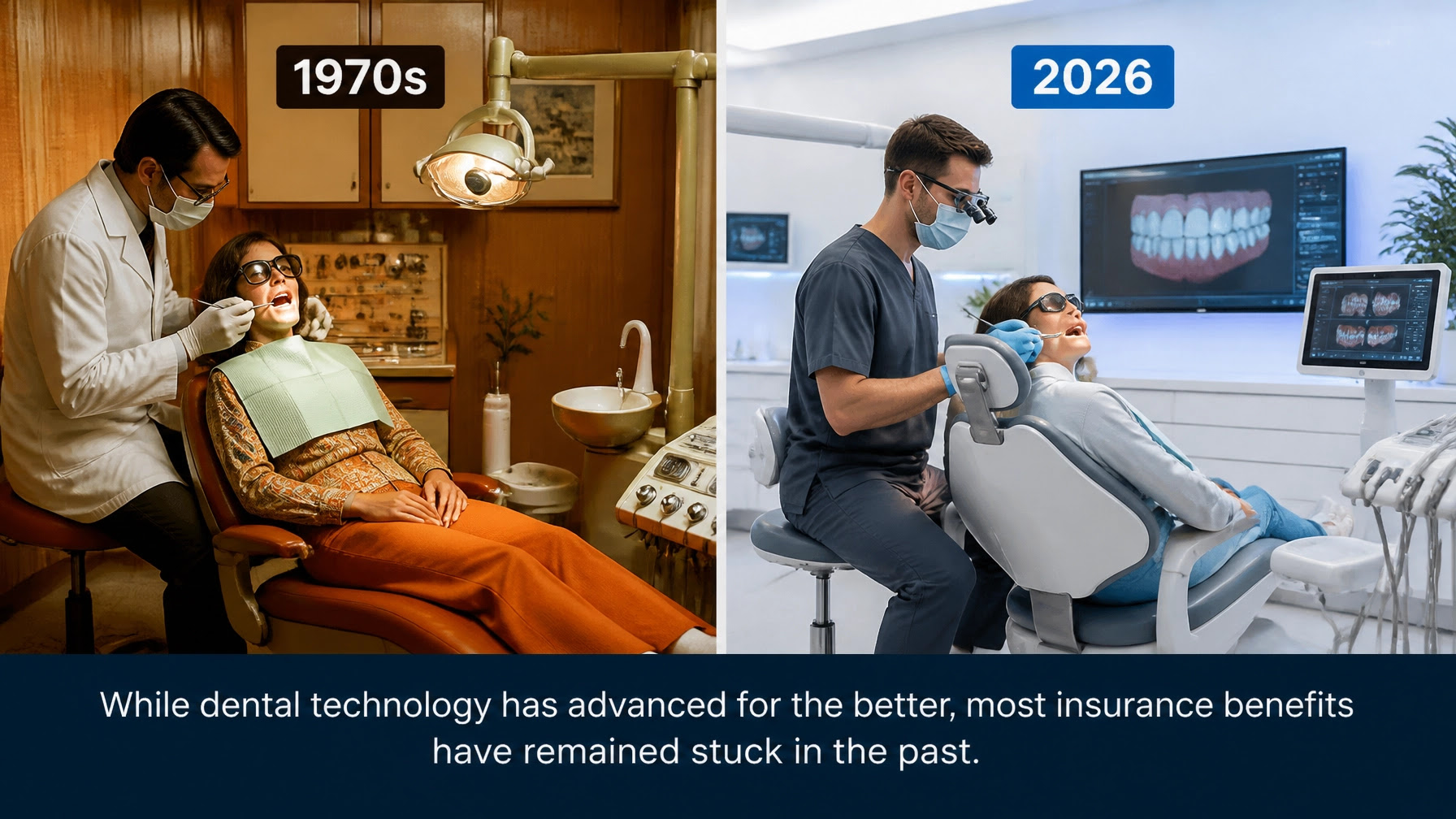

Fast forward to 2026.

We have digital scanners, 3D-printed teeth, and AI-powered diagnostics. But guess what hasn't changed? That same $1,500 annual maximum.

It’s the dental industry’s version of a bad joke, except nobody is laughing, especially not the practice owners and office managers who have to explain to a patient why their "premier" insurance plan barely covers a single tooth.

The Math That Should Make You Mad

If we actually adjusted that 1970 benefit for inflation, where should we be today?

Spoiler: It’s not $1,500.

According to current Consumer Price Index data, $1,500 in 1970 has the same buying power as nearly $13,000 today.

Let that sink in for a second. If dental insurance had actually kept pace with the real world, your patients would have a $13,000 yearly credit line for their oral health. Instead, they’re stuck with a "benefit" that has lost 88% of its value over the last five decades.

The insurance companies know this. They aren't "forgetting" to update their caps; they’re intentionally clinging to a Nixon-era standard to protect their bottom line while yours takes the hit.

Translation: What They Say vs. What They Mean

Insurance companies are masters of corporate-speak. They’ve spent decades training patients to think of "maximums" and "downgrades" as laws of nature rather than arbitrary rules designed to save the carrier money.

Let’s pull back the curtain on some of our favorite insurance phrases:

> The Insurance Company Says: "We are committed to providing affordable access to quality oral healthcare for our members."

>

> The Real Translation: "We’ve figured out that if we don't raise our caps for 50 years, our profit margins look fantastic, and the dentists get to be the 'bad guys' when the bill comes due."

> The Insurance Company Says: "This procedure exceeds the patient's annual maximum benefit."

>

> The Real Translation: "Your patient needs $5,000 worth of work to save their smile, but we’re only going to chip in for the first $1,500 because we’re still living in the disco era."

> The Insurance Company Says: "We’ve downgraded this porcelain crown to a silver amalgam reimbursement to keep costs low for the group."

>

> The Real Translation: "We know you don't do amalgams anymore, but if we pay you for one, we save $400. Good luck explaining that to the patient!"

How This "Time Capsule" Benefit is Killing Your Practice

When patients see that $1,500 cap, they don't see a historical relic, they see a ceiling on their health.

They start thinking: "If the insurance company only covers $1,500, then I must not need more than $1,500 worth of work."

This is the psychological trap. It forces you and your treatment coordinators to fight an uphill battle against a patient's own "benefit" plan. You aren't just a clinician anymore; you’re a negotiator, an educator, and occasionally a therapist for people who feel betrayed by the "coverage" they pay for every month.

And for the practice? It’s a recipe for stagnancy. While your overhead, staff wages, supplies, rent, and technology, continues to skyrocket with 2026 inflation, your reimbursements are often tied to these archaic fee schedules.

If you aren't negotiating your PPO fees or optimizing your contracts, you are essentially agreeing to work for 1970s wages in a 2026 world.

Stop Asking "What Insurance Covers"

It’s time to change the conversation in your office. We need to move away from being "insurance-driven" and start being "health-driven."

When a patient asks, "Will my insurance cover this?" the answer shouldn't be a simple "yes" or "no." It should be: "Your insurance hasn't updated their standards since the moon landing, but here is what your teeth actually require to stay in your head."

Wait: maybe don't say it exactly like that (unless you’ve had a really long Monday). But the sentiment stands.

You have to empower your team to explain that insurance is a coupon, not a care plan.

3 Ways to Fight Back:

Fee Negotiation: If the insurance companies won't raise the annual maximum, you must ensure you are getting the highest possible reimbursement for every code you submit. At Veritas, we use a 7-step process to negotiate with PPO insurance companies, often increasing practice revenue by 10-35%.

Insurance Verification: Don't let your front desk get blindsided. For $17/hr, our verification services handle the dirty work of digging through these messy plans so you can give patients accurate out-of-pocket estimates before they sit in the chair.

The Health Conversation: Pivot every financial discussion back to clinical necessity. When a patient says "I’ll wait until my benefits reset in January," remind them that bacteria don't follow a fiscal calendar.

Take Back Your Practice

The insurance companies have had a good run. They’ve spent fifty years convincing the public that $1,500 is a reasonable amount of money for a year of healthcare.

It isn't. It’s an insult to your expertise and a disservice to your patients.

You didn't go to dental school to let a billion-dollar corporation in an office building three states away decide how you treat your patients. You are the expert. It’s time to start acting like it.

We know the "insurance games" better than anyone, and we’ve made it our mission to help dental practices safeguard themselves from this kind of systemic bullying. Whether it’s auditing your billing or navigating the complexities of crown and buildup claims, we’re the partner you need in the trenches.

Stop letting 1970 dictate your 2026 revenue.

Because if you’re still playing by their rules, you’ve already lost.